Investors are wrestling with uncertainty about a variety of economic questions. Is inflation under control yet? What will the Federal Reserve do next? Does a recession lurk around the corner?

In June, the answers to all of those questions proved unsatisfactory. It was a month when the central bank’s Federal Open Markets Committee (FOMC) finally called a cease-fire in its intense war on inflation. After raising rates at 10 consecutive FOMC meetings in 2022 and 2023, the Fed took no action in June.

For a time it seemed that perhaps the Fed had moved out of its hawkish phase, and that investors could look forward to the central bank reversing course in the near future. But Fed officials quickly made clear that they’re not done raising rates. When he testified to Congress in late June, Federal Reserve Chairman Jerome Powell hinted that more rate hikes loom, perhaps as early as the FOMC’s July 26 meeting.

“We’re at least close to where we think our destination is … and it only makes common sense to move … at a careful pace,” Powell, speaking in the characteristically noncommittal tone of a Fed chairman, told the Senate Banking Committee.

Investors faced a period of intense uncertainty early in the pandemic, followed by a couple years of outsized returns. The return to reality, and to economic uncertainty, underscores the wisdom of our focus on high yield investment opportunities with best-in-class operators across a variety of asset classes. The Real Asset Investor raises capital from accredited investors to acquire assets for cash flow, equity growth, tax benefits and diversification, giving investors options outside of conventional financial markets.

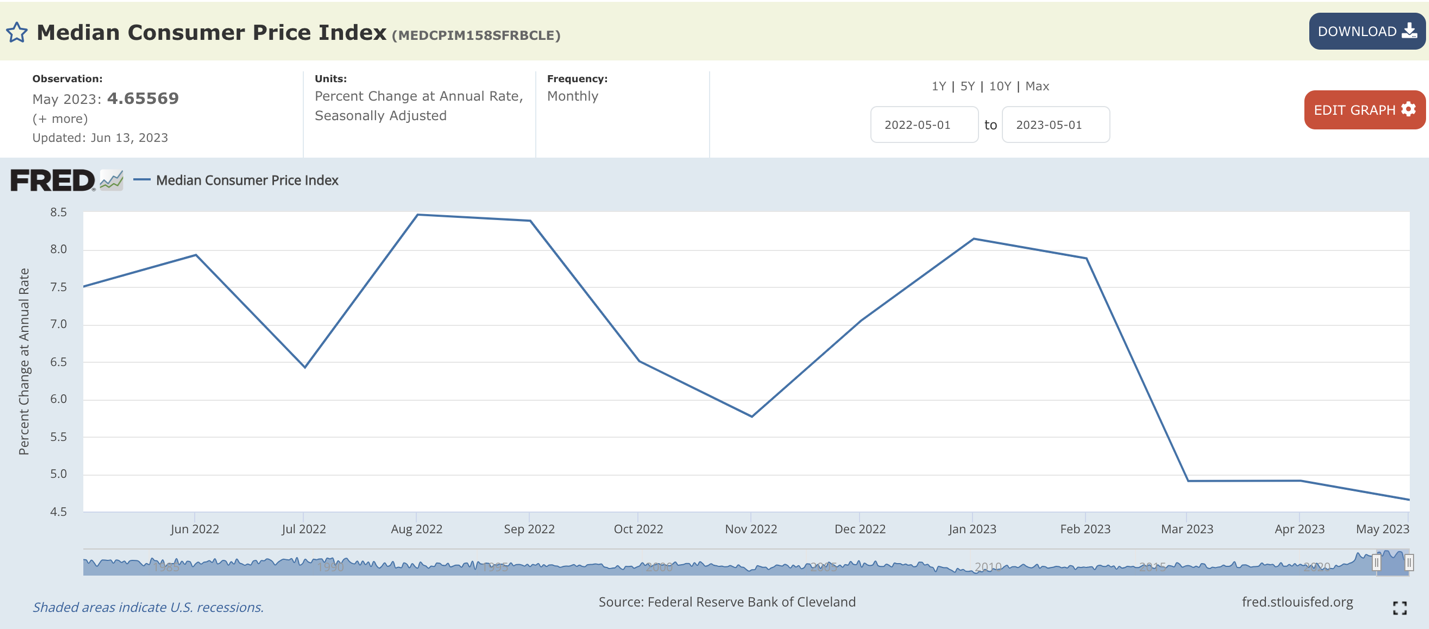

The inflation picture

The Fed, of course, is responding to a spurt of inflation spurred by the pandemic. To avert a full-blown depression, the Fed in 2020 slashed interest rates to zero, a policy echoed by central banks around the world. The Fed also began snapping-up mortgage-backed securities. And the U.S. government pumped trillions of dollars of stimulus into the economy.

All of that speedily delivered stimulus did indeed bolster the economy. Workers and employers quickly adapted by embracing remote work, and pharmaceutical companies rolled out effective vaccines faster than anyone expected. The result was an economic boom – and runaway inflation. By June 2022, the U.S. inflation rate topped 9%. It was the highest inflation since the stagflation days of the early 1980s.

But the Fed, after first denying the threat of inflation, quickly pivoted to inflation-fighting mode. From early 2022 through May 2023, it pushed rates from zero to 5%. And as of May 2023, the U.S. inflation rate had cooled to 4%, according to the Bureau of Labor Statistics.

The relationship between inflation and real estate values is a decidedly mixed bag. Inflation can lead to an increase in the value of real estate. This is because as the cost of goods and services increases, so does the cost of constructing new buildings. As a result, the value of existing buildings goes up, as those properties become more valuable relative to the cost of building new ones. What’s more, inflation can spur higher rents. On the downside, inflation leads to higher interest rates, which means the cost of borrowing to buy property goes up.

Overall economic activity

Despite continued predictions of a recession just around the corner, the labor market keeps humming along. In May, the U.S. economy created 339,000 jobs, a strong number. While unemployment rose to 3.7% from 3.4% the previous month, the economy remains at or near full employment.

There’s plenty of nuance in those numbers. For one, an increase in job openings caused the ratio of job openings to unemployed persons to increase. In addition, average hourly wages increased 0.3% month over month, and 4.3% year over year, to $33.44 an hour.

In another report, the U.S. Bureau of Economic Analysis revised gross domestic product (GDP) growth upward 0.2 percentage points to an annual rate of 1.3% for the first quarter of 2023. It’s the third consecutive quarter of positive GDP growth, although the pace is slowing. Along with the second estimate of GDP came the official first estimate of gross domestic income (GDI), which contracted by 2.3% in the first quarter of the year. The decline in GDI seems to forecast a potential slowdown in economic activity.

Indeed, a recession does seem to be looming, says Richard Barkham, chief global economist at real estate services firm CBRE. However, Barkham expects the coming downturn to be mild, and nothing like the Great Recession.

Barkham sees a number of factors propping up the U.S. economy. One is demography — population growth and a generational bulge of young, educated workers will spur output. So will an ever-evolving tech economy.

“I’ve seen four of these economic cycles, and this is by far the least serious,” Barkham told the National Association of Real Estate Editors in June.